ARTICLE | May 31, 2023

After two years of whipsaw change, Canada’s financial and commodity markets have entered a period of relative calm in recent months.

Volatility in the stock market has eased, oil prices have declined and the cost of raw materials has largely held steady. Even the elevated volatility in the bond market has begun to calm.

But lending conditions remain in restrictive territory, despite recent gains. It’s a reflection of the uncertainty over a slowing economy and elevated inflation, particularly among Canada’s trading partners, as well as other geopolitical tensions.

As a result, our proprietary RSM Canada Financial Conditions Index remains at 1.4 standard deviations below normal, indicating that greater risk than normal is being priced into financial assets.

This heightened risk shows up in the economy in the form of a greater reluctance to borrow or to lend, which ultimately leads to reduced economic activity.

RSM Canada Financial Conditions Index and Canada all-industries real GDP growth

Economists are now expecting Canadian gross fixed investment to decline by 2.7 per cent this year and for real gross domestic product to grow by less than 1 per cent.

The drop in investment can be attributed to the increase in the cost of capital and operating expenses brought about by higher interest rates around the globe.

Higher interest rates in both Canada and the United States have pushed 10-year government bond yields above the trading range (1 per cent to 2.5 per cent) of the low-inflation era.

Middle market insight

The increase in the central bank’s overnight interest rate quickly ended the era of minimal risk and financing on the cheap.

Although Canada’s inflation rate dropped from 8.1 per cent last June to 4.1 per cent in March, it is not yet at the Bank of Canada’s target range of 1 per cent to 3 per cent.

But with the labour market still tight and wages continuing to increase at a robust 4 per cent to 5 per cent annual rate, that target will remain elusive.

Although the Bank of Canada has left open the possibility that it will raise its policy rate again if inflation proves persistent, the forward markets are pricing in rate cuts by the end of the year.

In the end, it is the bond market that continues to be the main driver of increased risk in the RSM Canada Financial Conditions Index.

Canada and U.S. 10-year government bond yields

Monetary policy

The Bank of Canada has held its policy rate at 4.5 per cent since its last rate hike on Jan. 26. There has not been mention of a rate cut by the Bank of Canada, but rather the expected difficulty of reducing inflation from 3 per cent to the central bank’s 2 per cent target.

Yet the forward market thinks otherwise, expecting two rate cuts this year, one in September and one at the end of the year. According to the central bank, this could be in reaction to the likelihood of an economic contraction or in a more benign assumption that supply and demand will regain their balance, allowing inflation to soften.

The other half of central bank policy is its quantitative easing program. During a crisis, the bank purchases government securities, flooding the market with liquidity and simultaneously pressuring interest rates lower.

At the peak of its holdings, the bank’s balance sheet neared C$550 billion in assets, with outright holdings of government bonds reaching $430 billion by the end of 2021.

But the central bank has switched gears and is reducing its balance sheet. At its April 12 meeting, the central bank continued its current policy of normalizing the balance sheet by allowing maturing bonds to roll off. That is, those bonds are unlikely to have an effect on interest rates.

Bank of Canada holdings of assets

WEEKLY BALANCE SHEET BY TYPE OF SECURITY THROUGH APRIL

Quantitative tightening’s impact

This policy, known as quantitative tightening, began in February 2022, in the weeks before the Bank of Canada started to raise its overnight policy rate. The yield on 10-year bonds rose from 1.9 per cent to 3.2 per cent in less than three months on the realization that inflation was anything but transitory.

By November 2022, 10-year yields were beginning a jagged path to as high as 3.6 per cent, only to fall to less than 3 per cent at the end of April 2023.

There were other factors at play, with the shock of inflation and the possibility of an economic downturn playing bigger roles than the maturing of securities in the determination of bond yields.

Bank of Canada holdings of government bonds and 10-year bond yields

Lending conditions

The Bank of Canada’s quarterly survey of bank lending conditions offers another view of the transmission of monetary policy to the real economy through financial conditions.

As of the fourth quarter, overall bank lending had become restrictive in response to the increased cost of financing commercial and consumer loans.

The increase in the central bank’s overnight interest rate quickly ended the era of minimal risk and cheap financing. Lenders suddenly had a lot more to lose and therefore increased their lending standards.

We expect this trend to continue for as long as the Bank of Canada maintains or raises its policy rate.

Canada lending conditions and real GDP growth by expenditure

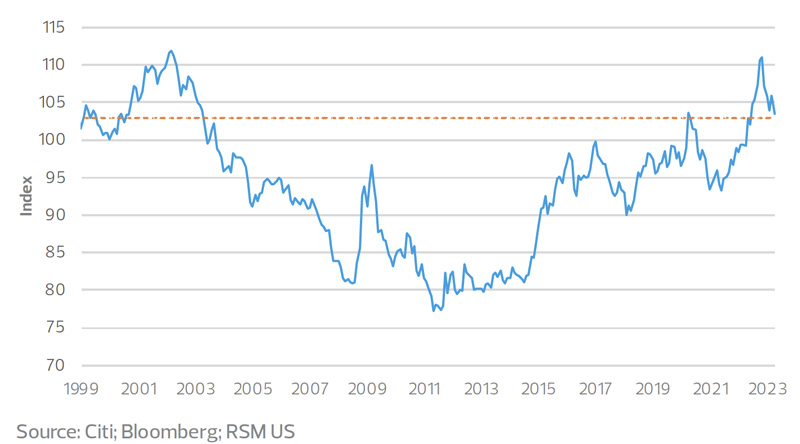

The Canadian dollar

The Canadian dollar remains a commodity currency, rising and falling with the value of its resources. Its peak in the spring of 2022 coincided with the dramatic shift in monetary policy and the tightening of financial conditions.

It is true that the increased value of the Canadian dollar and commodity prices in 2021 until March of last year coincided with the recovery from the health crisis and the increased demand for commodities, particularly energy.

But we would argue that there were other reasons for that increase, including the reduced supply of goods and a surge in shipping costs.

Eventually, shipping costs eased along with the pandemic and its recurring waves. And fears of energy shortages in Europe were averted by a mild winter and a comprehensive effort to find alternative sources.

Now, with commodity prices approaching a normal range and barring another crisis, we can assume that a slowdown in global growth will result in lower demand for raw materials and a moderated value of the Canadian dollar.

Commodity prices and Canadian dollar index

Let’s Talk!

Call us at 1 855 363 3526 or fill out the form below and we’ll contact you to discuss your specific situation.

This article was written by Joe Brusuelas and originally appeared on 2023-05-31. Reprinted with permission from RSM Canada LLP.

© 2024 RSM Canada LLP. All rights reserved. https://rsmcanada.com/insights/economics/tighter-financial-conditions-threaten-canadas-growth.html

RSM Canada LLP is a limited liability partnership that provides public accounting services and is the Canadian member firm of RSM International, a global network of independent assurance, tax and consulting firms. RSM Canada Consulting LP is a limited partnership that provides consulting services and is an affiliate of RSM US LLP, a member firm of RSM International. The member firms of RSM International collaborate to provide services to global clients but are separate and distinct legal entities that cannot obligate each other. Each member firm is responsible only for its own acts and omissions, and not those of any other party. Visit rsmcanada.com/about for more information regarding RSM Canada and RSM International.