ARTICLE | March 18, 2024

First published by the Canadian Tax Foundation and the International Fiscal Association in (2024) 3:1 International Tax Highlights 5-7.

Executive Summary

On Nov. 21, 2023, Canada signaled its intention to proceed with proposed hybrid mismatch arrangement (HMA) rules, now forming part of Bill C-59. In this article, we address whether the first package of legislative proposals related to the HMA rules will, along with the pending second package, have an impact on the use of the unlimited liability company structure for conducting business in Canada from the United States. We use three examples to help illustrate our consideration of whether certain deductible expenses would be disallowed in Canada under the HMA rules.

On Nov. 21, 2023, Canada signaled its intention to proceed with proposed hybrid mismatch arrangement (HMA) rules. More recently, on Nov. 28, 2023, Canada released the notice of ways and means motion that includes the first package of the revised HMA legislation. This now forms Bill C-59, tabled before the House of Commons. The first package of the proposed legislation implements the recommendations included in chapter one of the Organization for Economic Co-operation and Development (OECD) Base erose and profit shifting (BEPS) action 2 final report, addressing deduction/non-inclusion (D/NI) mismatches that arise from payments under (1) hybrid financial instrument arrangements, (2) hybrid transfer arrangements and (3) substitute payment arrangements. The first package also implements some of the recommendations in chapter two of the action 2 final report, addressing dividend deductions under section 113 to the extent that they are deductible under foreign law. A retroactive date of July 1, 2022 is provided for most elements of the first package. Other recommendations of the BEPS action 2 report will be included in the second package of the proposed legislation, which has not been released as of this writing.

In this article, we address whether the first package of legislative proposals related to the HMA rules will, along with the pending second package, have an impact on the use of the unlimited liability company (ULC) structure for conducting business in Canada from the United States. We use three examples to help illustrate our consideration of whether certain deductible expenses would be disallowed in Canada under the HMA rules.

Use of Canadian ULCs for carrying on business in Canada from the United States

Generally, Canadian ULCs are created by provincial statute in Canada. They may yield certain benefits when they are used for carrying on business in Canada. A ULC is treated as a flowthrough entity by default for US tax purposes (unless an election is made to treat the ULC as a corporation), and it is treated as a corporation in Canada, subject to regular Canadian corporate tax. From a US perspective, the benefits of Canadian ULCs may include the ability to operate in a branch form for US tax purposes while maintaining the legal protection of two distinct corporations and the ability to apply Canadian operating losses against a US parent’s taxable income.

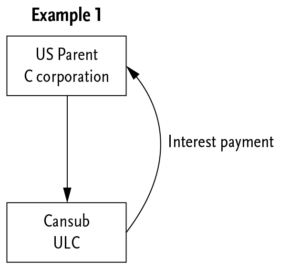

Example one

In example one, a US C corporation (“US Parent”) has a wholly owned subsidiary in Canada (“Cansub”). Cansub is a ULC that is treated as an opaque entity in Canada but as a disregarded entity in the United States. Cansub received an interest-bearing loan from US Parent. The interest payments are deductible in Canada by Cansub. However, since Cansub is a disregarded entity in the United States, there would be no corresponding income inclusion in that country. This structure is already affected by the denial of withholding tax relief under the Canada-US tax treaty (“the treaty”) because of article IV(7)(b), but, for the moment, let us just consider the additional implications.

First package of the proposed legislation

Under proposed subsection 18.4(10), a payment will arise from a hybrid financial instrument arrangement if the following four conditions are met:

- the payment arises under, or in connection with, a financial instrument;

- the payer and the recipient are either non-arm’s-length or specified entities, or the arrangement is a structured arrangement;

- the payment gives rise to a D/NI mismatch; and

- it can reasonably be considered that (a) the D/NI arises (in whole or in part) because of a difference between two or more countries in their tax treatment of either the financial instrument or transactions that are related to the financial instrument, and (b) this difference is attributable to the terms or conditions of the financial instrument or other relevant transactions.

If a payment arises from a hybrid financial instrument arrangement (one of three HMAs), the primary operative rule in subsection 18.4(4) will restrict a deduction in Canada that results in a D/NI mismatch.

In example one, there is a deduction in Canada but no recognition of income in the United States, resulting in a D/NI mismatch.

However, several arguments may be advanced to alleviate concerns that an overly broad reading of this first HMA legislative package applies to structures with a hybrid entity. First, the D/NI mismatch in example 1 arises primarily because of the difference between the countries in their tax treatment of Cansub (that is, regarded/disregarded), not because of a difference in the tax treatment of the financial instrument as such. Second, under the interpretation rule in proposed subsection 18.4(2), the Canadian rules are to be interpreted in accordance with the OECD’s action 2 report. In that report, in the overview section of chapter 1 (on which Canada’s first package of legislation is partly based), it is stated that “[a] payment cannot be attributed to the terms of the instrument where the mismatch is solely attributable to the status of the taxpayer or the circumstances in which the instrument is held.” Third, the explanatory notes provided by Finance for the proposed legislation include several examples—including examples of (1) structures with notional interest expenses on non-interest-bearing loans, (2) forward subscription agreements paired with loans, and (3) sale and repurchase agreements —and the OECD’s action 2 report provides 37 examples, and none of these examples, with respect to hybrid financial instruments, detail a mismatch arising solely because the entity is classified differently in two countries.

Second package of the proposed legislation

The second package of the proposed legislation has not been released. It is expected to include other recommendations of the BEPS action 2 report. Chapter three of the report (“Disregarded Hybrid Payments Rule”) targets a deductible payment, made by a hybrid entity, that is disregarded under the laws of the payee jurisdiction and is therefore not treated as income under the laws of the payee jurisdiction. The purpose of this rule is to prevent a taxpayer from exploiting differences between jurisdictions in the tax treatment of the payer entity. The primary recommendation in chapter 3 of the report is that the payer jurisdiction should restrict the amount of the deduction, and the defensive rule requires that the payee jurisdiction include an equivalent amount in ordinary income.

Furthermore, chapter three provides that no mismatch will arise to the extent that the payer’s deduction is set off against dual-inclusion income. “Dual-inclusion income” is generally defined in the BEPS action 2 report as an income item that is included in income under the laws of both the payer and payee jurisdictions. In addition, double taxation relief, such as a foreign tax credit granted by the payee jurisdiction, “should not prevent an item from being treated as dual inclusion income where the effect of such relief is simply to avoid subjecting the income to an additional layer of taxation in either jurisdiction” (at paragraph 126). Significantly, implementation techniques may vary by country; however, the BEPS action 2 report recommends (at paragraph 126) that when a determination is being made as to whether to treat as dual-inclusion income an item of income that benefits from double taxation relief, an approach should be taken that balances rules that “minimise compliance costs, preserve the intended effect of such double taxation relief and prevent taxpayers [from undermining] the integrity of the rules.”

If Finance were to implement, in the legislation’s second package, the recommendations in chapter 3 of the action 2 report, the arrangement described in example 1 (above) might be affected, and the deduction for interest expense might be disallowed in Canada to the extent that Cansub is in a net loss position. A deeming rule could be introduced to deem the interest payment to be a dividend paid to US Parent (a rule similar to proposed subsection 214(18) in the first package). The deemed dividend might be subject to a withholding tax of 25% because of the anti-hybrid provision in article IV(7)(b) of the treaty.

Remedial steps

If the second package of the proposed legislation indeed has an impact on the ULC structure, a remedy might be to convert the ULC to a regarded entity for US tax purposes.

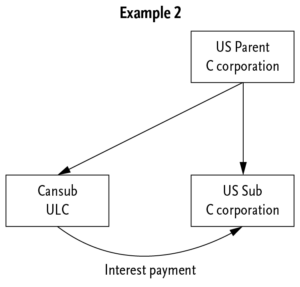

Example two

In example two, which is a variation on example one, the loan is made by a US subsidiary of US Parent (“US Sub”), and US Sub is a C corportion. The interest payments are deductible both by Cansub in Canada and by the US Parent in the United States. US Sub will have an income inclusion in the United States from the interest income. In this example, we have assumed that the indebtedness originates from US Sub. In particular, the US Parent did not loan the funds to US Sub in order to further the loan to Cansub.

Variations on the intercompany loan structure shown above are commonly employed to avoid the application of article IV(7)(b) of the treaty and to access treaty benefits on the interest payment, on the basis that the treatment of the interest for US tax purposes is the same as the treatment that would result if the ULC were not a fiscally transparent entity. (In Canada Revenue Agency (CRA) document no. 2010-0376751E5, May 24, 2011, the CRA compared the two treatments, considering, in both scenarios, the quantum, character, and timing of the item of income under US tax laws.)

First package of the proposed legislation

For the same reasons that applied with respect to example one, it is arguable that the first package of the proposed legislation may not apply.

Second package of the proposed legislation

As discussed above, the second package of the proposed legislation, which has not yet been released, will include other recommendations of the BEPS action 2 report. In particular, chapter 6 of the report (“Deductible Hybrid Payments Rule”) would apply to a “hybrid payer” that makes a payment that (1) is deductible under the laws of the payer jurisdiction and (2) triggers in the parent jurisdiction a duplicate deduction that results in a hybrid mismatch. A “hybrid mismatch” will occur if a deduction may offset income that is not dual-inclusion income. A person will be a “hybrid payer,” according to chapter six, where

- a payment is deductible under the laws of the payer jurisdiction,

- the payer is resident in the payer jurisdiction, and

- the payment triggers a duplicate deduction for an investor in that payer (or in a related person) under the laws of the other jurisdiction (the parent jurisdiction).

Importantly, chapter six provides that the rule will not apply if a deduction can be offset against an amount that will be included in income in both jurisdictions. This means, in the case of example two, that if the interest expense can be offset against income of Cansub (which will be taxed in both Canada and the United States), the rule may not apply. If Cansub is in a loss position, however, chapter 6 may apply.

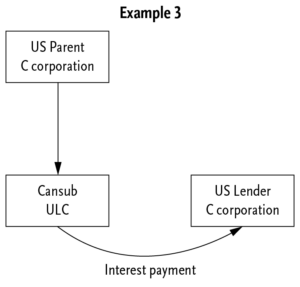

Example three

Example three is the same as example two, except that Cansub now receives a loan from a third party. The interest payments are deductible both by Cansub in Canada and by the US Parent in the United States.

First package of the proposed legislation

One of the conditions that must be met, in order for the arrangement to be considered a hybrid financial instrument arrangement, is that the payer and the recipient are either non-arm’s-length entities or specified entities, or that the arrangement is a structured arrangement. Since the lender in example three is a third party, the payer and the recipient would not be either specified entities or non-arm’s-length entities. A structured arrangement is defined, in general terms, as a transaction that gives rise to a D/NI mismatch, in a situation where it can reasonably be considered that a portion of the economic benefit arising from the D/NI mismatch is reflected in the pricing of the transaction that gives rises to a D/NI mismatch, or the transaction or series was otherwise designed to give rise to the D/NI mismatch.

Assuming that the loan is not a structured arrangement, it would not be considered a hybrid financial instrument arrangement and would not be caught by the first package of the proposed legislation.

Second package of the proposed legislation

Chapter 6 of the BEPS action 2 report is relevant for this example, and the chapter 6 recommendations may be implemented by Finance in the second package of the legislation; therefore, it is important to understand whether chapter 6 applies to arrangements between arm’s-length parties. The overview for chapter six of the action 2 report includes a proposed scoping rule that enforces, notably, only the defensive aspect of the rule: it denies a deduction in the payer jurisdiction (that is, in Canada). According to the action 2 report, the scoping rule restricts the application of the deduction denial to situations where parties are in the same control group or are part of a structured arrangement. Therefore, if the loan in example three is not a structured arrangement, chapter six may not apply to it, and the interest deduction may not be disallowed in Canada.

Next steps

Further analysis will have to be undertaken once Finance releases the second package of HMA rules. In the meantime, this article has proposed that the structures herein described, along with similar structures, may be safe from the application of the first package of proposed legislation.

Let’s Talk!

Call us at 1 855 363 3526 or fill out the form below and we’ll contact you to discuss your specific situation.

Source: RSM Canada LLP.

Reprinted with permission from RSM Canada LLP.

© 2024 RSM Canada LLP. All rights reserved. https://rsmcanada.com/insights/services/business-tax-insights/can-the-hybrid-mismatch-rules-affect-canadian-ulcs.html

RSM Canada LLP is a limited liability partnership that provides public accounting services and is the Canadian member firm of RSM International, a global network of independent assurance, tax and consulting firms. RSM Canada Consulting LP is a limited partnership that provides consulting services and is an affiliate of RSM US LLP, a member firm of RSM International. The member firms of RSM International collaborate to provide services to global clients but are separate and distinct legal entities that cannot obligate each other. Each member firm is responsible only for its own acts and omissions, and not those of any other party. Visit rsmcanada.com/about for more information regarding RSM Canada and RSM International.