Your Business News

Global insurance accounting practices converge

November 4, 2022

Authored by RSM Canada LLP

Kirby W. Houle, CPA, CA shared this article

ARTICLE | November 04, 2022

With the effective date of the International Accounting Standards Board’s insurance contracts standard—known as IFRS 17—and U.S. generally accepted accounting principles long-duration targeted improvements (LDTI) for many insurers approaching Jan. 1, 2023, global insurance accounting and actuarial practices are becoming more aligned than ever. However, significant differences remain between IFRS 17 and LDTI, and these discrepancies could affect insurance companies’ financial results and capital.

From 2023 onward, for many insurers the interpretation of enterprise financial performance within and outside the United States will require understanding the differences between IFRS 17 and LDTI. Though the standards are based on similar concepts, their differing measurement and reporting requirements may give rise to significant differences in the timing, presentation and disclosure of profit emergence.

Translation between the changes in IFRS 17 and LDTI may require changes to financial reporting accounting processes, actuarial models, data management, and systems architecture. Insurers should take action now to understand the nuances of these two standards and their implications for portfolios, discount rates, risk adjustments and more.

Insurance contract portfolios (IFRS 17 (14-24))

Paragraphs 14 through 24 in section 17 of the IFRS—the International Financial Reporting Standards—introduced a new accounting concept called the insurance contract portfolio. A portfolio is defined as a collection of insurance contracts subject to similar risks and managed together. Additionally, contract groups are identified as a unit of measurement within portfolios. IFRS 17 groups are distinguished by profitability characteristics, and contracts within a group cannot be issued more than one year apart.

LDTI maintains quarterly or annual groups (known as cohorts); and similar to IFRS 17, contracts issued in different years cannot be grouped. LDTI, though, does not require contract groups to be separated based on profitability characteristics.

Assessing and separating insurance contracts into annual groups may present operational challenges. For example, multiple separate cohorts will require assessment on a continuing basis because IFRS 17 and LDTI both prohibit entities from including contracts issued more than one year apart in the same group. Insurers who report both in the United States and internationally may need to introduce new data elements to enable filtering and aggregation of contracts. The transition from LDTI into IFRS 17 will require that annual cohorts be identified as either onerous or profitable groups.

Operationally, insurers may need to adopt new methods to process new types of data, transfer the data into actuarial systems and measure that information. Governance processes around model change management may become a focal point.

Accounting for longer vs. shorter coverages (IFRS 17 (53))

IFRS 17 and LDTI both distinguish between long duration and shorter duration contracts. For example, IFRS 17 introduced a new general measurement model (GMM) (IFRS 17 (32-52)) is typically applied to longer duration contracts, while the alternative premium allocation approach (PAA) is allowed for contracts with one year of coverage or less.

LDTI also differentiates between long and shorter duration contracts, although its specifics of how to do so differ from IFRS 17.

Acquisition costs

IFRS 17 requires acquisition costs to be deferred under the GMM and provides an accounting policy choice of deferral or expense under the PAA. Additionally, IFRS 17 defines insurance acquisition costs for the first time, which may result in new costs for insurers.

LDTI eliminates current U.S. GAAP methods of amortizing in proportion to profit measures such as premiums (traditional life), estimated gross profits (nontraditional) or estimated gross margins (participating life). Instead, LDTI requires insurers to amortize deferred acquisition costs on a constant-level basis over the expected life of the contracts, independent of profitability or revenue considerations.

Insurers may need to update their systems and processes to transfer new types and amounts of acquisition costs into their accounting systems and actuarial measurement models. They also will need to allocate new types of acquisition costs and amortization periods into new periods, portfolios and cohorts.

Risk adjustment (IFRS 17 (32(a)(iii), 37))

IFRS 17 risk adjustment is an explicit part of insurance liability and contributes to profits under both the GMM and PAA approaches. The new risk adjustment calculation represents the compensation an entity requires for bearing the uncertainty about the amount and timing of nonfinancial risk cash flows. This calculation is complex and may require insurers to build new actuarial models and processes.

Under IFRS 17, approaches to calculating risk adjustment include the percentile method and the cost of capital method. The equivalent insurance measurement under the current U.S. GAAP is the provision for adverse deviation (PAD), which follows a different methodology compared to IFRS 17 approaches. However, under LDTI, the PAD requirement is removed in the calculation of future policy benefits.

Discount rates (IFRS 17(36))

IFRS 17 and LDTI have technical differences in their approaches to discounting, with significant implications for profitability and capital. Under IFRS 17, insurance contract claims expected to be settled in more than 12 months are required to be measured at the discounted value, similar to previous practices under IFRS. However, IFRS 17 also introduces a fundamentally different approach to calculating the discount rate used for the valuation of insurance liabilities. The standard requires application of either the top-down (IFRS 17 (B81)) or bottom-up (IFRS 17 (B80)) approach to calculate the discount rate. The discount rates are required to reflect the characteristics of underlying insurance contracts.

In contrast, LDTI requires insurers to set the discount rate using an upper-medium grade (generally interpreted as single-A or equivalent rating) fixed-income instrument yield in subsequent accounting periods, reflecting the duration characteristics of the liability and maximizing the use of observable inputs. As a result of this guidance, the calculation will incorporate single-A rates for each cash flow duration. Under LDTI, the impact of changes to discount rates will be reflected in other comprehensive income.

Cash flow assumptions

Changes in assumptions can have significant impacts on the valuation of insurance contracts and are often subject to significant scrutiny and oversight. IFRS 17 generally maintains previous IFRS approaches, in which significant assumptions are updated at each balance sheet date to arrive at best estimates of future cash flows.

LDTI aligns with IFRS 17 by introducing requirements for best estimates, requiring insurers to review and update the assumptions on at least an annual basis to reflect current experience. Under LDTI, the impact of updating cash flow assumptions (other than the impact of the change in discount rate) will be reflected in earnings.

Presentation and disclosure (IFRS 17 (78-132))

IFRS 17 and LDTI both have new disclosure requirements, which generally expand the quantity of information required compared to previous requirements. IFRS 17 condenses the presentation of insurance contracts within the financial statements and expands disclosure tables to include new elements of measurement within the GMM and PAA accounting approaches.

LDTI similarly expands disclosures to include year-to-date disaggregated roll-forward tables, providing an increased level of transparency for users of the financial statements.

Further considerations

Integration of IFRS 17 and LDTI changes will require greater interaction between actuarial and accounting systems and functions and involve significant challenges around data, modeling, processes governance and business integration. RSM can help you take advantage of the opportunities arising from changing requirements. Our experienced teams of actuaries, consultants, IT managers and other professionals can help you empower your business to deliver on its potential and embrace the possibilities.

Market risk benefits

IFRS 17 and LDTI differ most in their consideration of the market risk benefit (MRB). LDTI created the MRB—a new classification of liability—and defines it as a benefit feature that protects the policyholder’s account balance from and exposes the insurer to more than nominal capital market risk. LDTI requires insurers to measure the MRB at fair value to improve uniformity for measuring similar benefit features among different insurers; hence this change may not significantly affect some insurers that already use the fair value approach for similar existing guarantees.

In contrast, IFRS 17 does not define MRB or a method of measurement, but requires insurers to reflect a market-consistent value of options and guarantees within the measurement of fulfilment cash flows.

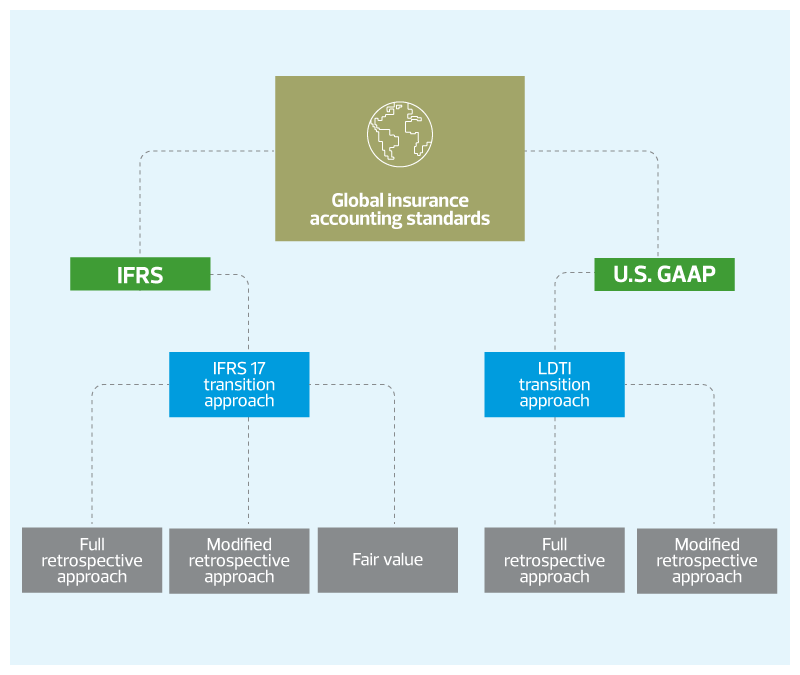

Transition (IFRS 17, appendix C)

Transition approaches to IFRS 17 and LDTI are similar, but important differences can affect profitability and capital. For example, the IFRS 17 effective date is Jan. 1, 2023. While that is also the LDTI transition date for publicly listed insurance companies (not qualifying as a smaller reporting company), all other entities—including privately held insurance companies—have until Jan. 1, 2025 to transition.

The selected transition approach determines the measurement of insurance liability. IFRS 17 outlines three approaches that vary according to an insurer’s circumstances. The full retrospective approach (IFRS 17 (C3)) requires a full restatement as if the standard had always been applied since issuance of the insurance contracts. The modified retrospective (IFRS 17 (C6)) and fair value (IFRS 17 (C20)) approaches can be used where the full retrospective approach cannot be applied.

LDTI permits only two approaches to transition: full retrospective approach or modified retrospective approach, the latter with an exception that an MRB must be measured at fair value on the transition date using the full retrospective approach.

Insurers operating in both the United States and internationally will need to closely examine the merits of and differences between these transition approaches.

Further considerations

Adoption of IFRS 17 and LDTI will require greater interaction between actuarial and accounting systems and functions and involve significant challenges around data, modeling, process governance and business integration. RSM can help you take advantage of the opportunities arising from these changing requirements. Our experienced teams of actuaries, consultants, IT and other professionals can empower your business to deliver its potential and embrace the possibilities.

Let's Talk!

Call us at 1 855 363 3526 or fill out the form below and we'll contact you to discuss your specific situation.

This article was written by Liam Neilson, Jake Seok, Craig Cross and originally appeared on Nov 04, 2022 RSM Canada, and is available online at https://rsmcanada.com/insights/industries/insurance/global-insurance-accounting-practices-converge.html.

RSM Canada Alliance provides its members with access to resources of RSM Canada Operations ULC, RSM Canada LLP and certain of their affiliates (“RSM Canada”). RSM Canada Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each are separate and independent from RSM Canada. RSM Canada LLP is the Canadian member firm of RSM International, a global network of independent audit, tax and consulting firms. Members of RSM Canada Alliance have access to RSM International resources through RSM Canada but are not member firms of RSM International. Visit rsmcanada.com/aboutus for more information regarding RSM Canada and RSM International. The RSM trademark is used under license by RSM Canada. RSM Canada Alliance products and services are proprietary to RSM Canada.

FCR a proud member of RSM Canada Alliance, a premier affiliation of independent accounting and consulting firms across North America. RSM Canada Alliance provides our firm with access to resources of RSM, the leading provider of audit, tax and consulting services focused on the middle market. RSM Canada LLP is a licensed CPA firm and the Canadian member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM Canada Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise, and technical resources.

For more information on how FCR can assist you, please call us at 1 855 363 3526